Most operators were trained to balance a dashboard (a row of co-equal numbers, all of them now easier to move). But they were never co-equal. One of them was always the river the rest juMost operators were trained to balance a dashboard (a row of co-equal numbers, all of them now easier to move). But they were never co-equal. One of them was always the river the rest just feed.

For most of my career, the honest answer to “what does a senior operator actually serve” would have been: that dashboard. Revenue, CAC, NPS, utilization, velocity, retention (balance them, keep them all healthy). That model just broke. Twice.st feed. For most of my career, the honest answer to "what does a senior operator actually serve" would have been: that dashboard. Revenue, CAC, NPS, utilization, velocity, retention (balance them, keep them all healthy). That model just broke. Twice.

Why the dashboard broke. First, AI made most of those metrics cheap to move. When you can spin up campaigns, ship features, and generate analysis at low marginal cost, optimizing any single metric in isolation stops being a signal and becomes motion. When every number on the board moves with a prompt, a balanced dashboard tells you almost nothing. It’s noise with good design.

Second, and this is the one we’ve been trained not to see: those metrics were never co-equal to begin with. We just lived through an era that let us pretend they were.

We were trained on an anomaly. Look at a long-run chart of the S&P and you’ll see a line that, through every crash and recession, only really knows one direction: up. That’s the experience the last 50 years burned into business (especially the last fifteen). From roughly 2009 to 2021, money was easy. Capital was cheap, abundant, and the next round felt certain.

That environment taught a generation of operators a single, distorting lesson: growth is rewarded, burn is forgivable, and cash is a detail finance handles in the basement. “Grow fast, raise the next round, fix the unit economics later” wasn’t stupid. In a world of free money, it was rational. But that was the tailwind doing the work, and a tailwind isn’t a law of business. Cheap, abundant liquidity is the historical exception. For most of economic history capital was scarce and expensive, and the operators who survived were the ones who managed one thing above all: the speed at which money came back through the door.

It’s the oldest constraint there is. Even empires run on it. Napoleon’s march into Russia was, at its core, a supply-and-logistics collapse (the most powerful army in the world couldn’t keep itself fueled far from home). Rome’s long decline was, among other things, a fiscal one (an overstretched treasury that could no longer pay for what it had built). Strip away the romance and the lesson is plain: it doesn’t matter how strong the machine looks if it runs out of fuel. We just spent fifteen years with the luxury of forgetting that the fuel has a name. It’s cash.

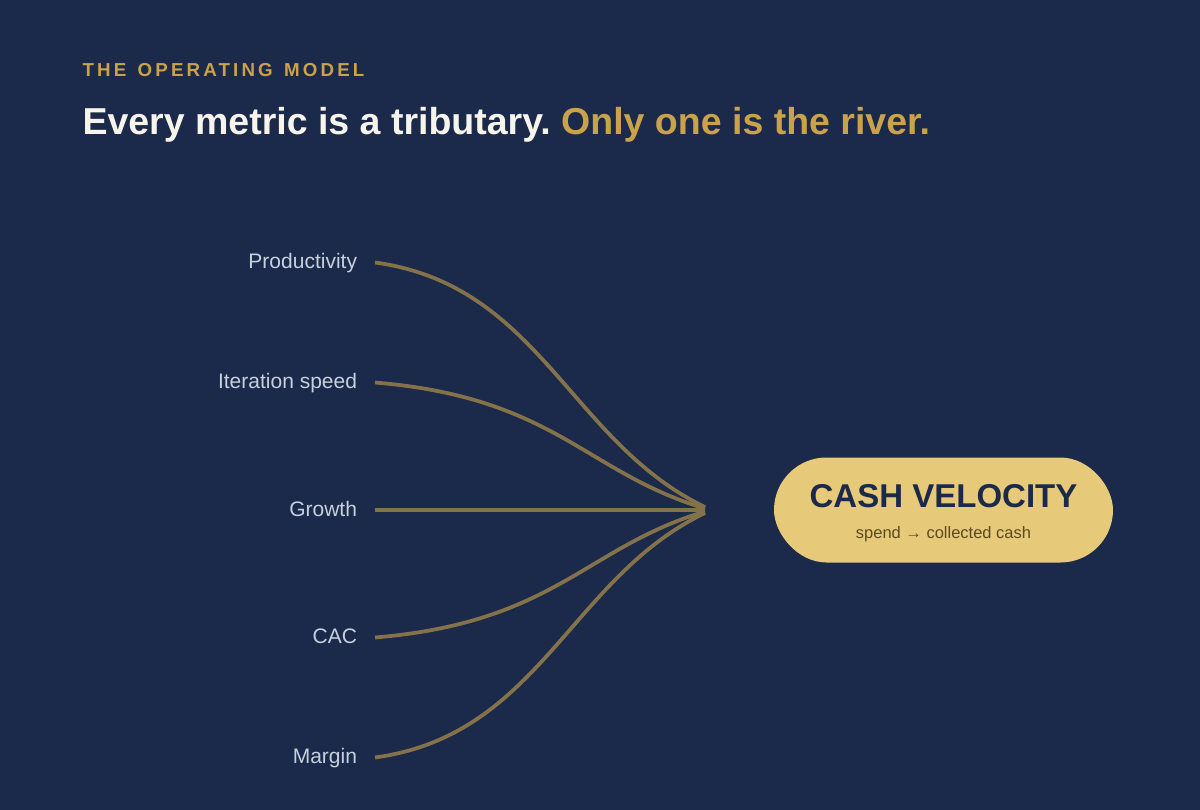

Cash velocity is the master KPI. So here’s the reframe the AI-native operator runs on. Cash conversion (how fast a dollar of spend becomes a dollar of collected cash) sits above the rest. It’s the master metric, and everything else is a tributary feeding it.

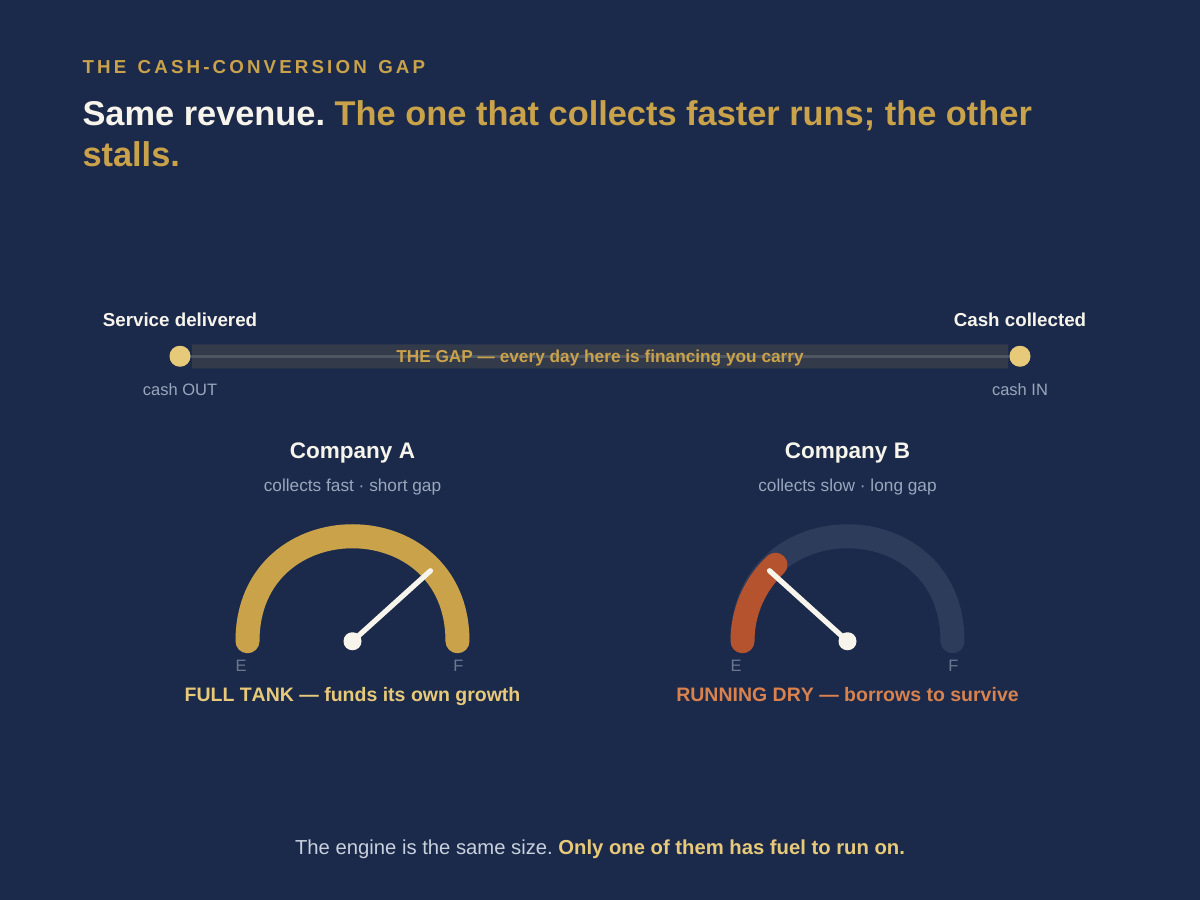

Make it concrete. A clinic delivers care today, bills a payor, and collects the cash 60, 90, sometimes 120 days later (if the claim isn’t denied and reworked first). Every dollar of that delay is a dollar the business has to fund some other way while it waits. The gap between service delivered and cash collected is the difference between a company that funds its own growth and one that has to borrow to survive its own success (even when the two post identical revenue). That gap (not the revenue line) is the game. It shows up everywhere money goes out before it comes back: a payor reimbursement loop, a DTC brand’s inventory-and-ad spend, a distributor’s terms with its channel and suppliers.

Productivity matters because it shortens the distance between spending and collecting. Iteration speed matters because faster loops find the cash-generating motion sooner (and, just as important, kill the cash-burning ones before they drain you). Growth itself is only good cash judgment when it returns more than it consumes, on a timeline you can survive.

This is what gives the new operator their actual shape. The orchestrator’s job goes past keeping a dashboard balanced. It’s to route every fast-moving function toward cash velocity (and to know, in real time, which iterations feed the cash engine and which merely feel productive). That distinction is the whole job. In a cheap-money world you could blur it for years. You can’t anymore.

AI makes this truer. Here’s the part that closes the loop. The same force that collapsed the cost of execution is, at the macro level, concentrating the cost of capital. The AI buildout (data centers, power, chips) is one of the most capital-hungry undertakings in modern history. The four largest hyperscalers alone plan around $725 billion in capital spending in 2026 (up roughly 77% in a single year), and it’s denting even their famously deep pockets, with Amazon projected to turn free-cash-flow negative. When the richest companies on earth are feeling the cash squeeze of their own buildout, the capital it pulls toward itself gets scarcer and more expensive for everyone else.

Read that slowly: building is getting cheap while the ground you build on is getting expensive, and the capital to fund it is no longer easy. Treat it as a recession to wait out and you’ll miss the point. It’s the operating condition of the era we’re entering. So cash discipline stops being a downturn skill and becomes the baseline competency of the AI age.

The version that's true whichever way it breaks. I’ll be straight about the limit of this. I can’t forecast the macro, and neither can anyone selling you certainty about it. Maybe AI’s productivity gains are large enough to grow us out of the squeeze and money loosens again. Maybe not. But notice the thesis doesn’t need the prediction. Cash velocity was always the master metric. The last era was simply an anomaly that let us forget it. Whichever way the next decade breaks, the operator who treats cash as the spine (who connects every accelerated function back to the speed of collected money) is the one who keeps the company alive long enough for all that cheap execution to compound.

"But sometimes you're supposed to burn." There’s a fair objection here, and it built some of the biggest companies of the last cycle. In winner-take-all markets, the rational move is to burn cash to capture the field (Uber, Amazon, the AI labs right now). But that was never permission to ignore cash. It was a forecasted, time-bound burn with a defendable moat at the end (a GTM line item with a model and an exit), valid precisely because the head start stayed protected long enough to harvest. AI breaks the back half of that structure. When the cost and time of catching up collapse, your lead stops being durable: the moment your subsidized position looks valuable, a competitor with the same models and faster iteration can replicate it before the burn ever pays off. The moat doesn’t set. Uber in 2010 could out-burn rivals into a defended network; launched into 2026, it gets cloned mid-burn. The one exception that seems to disprove cash discipline turns out to require the very thing AI just made cheap: a durable head start.

The dashboard had many numbers. There was only ever one that mattered. The operators who remember that first will be the ones still standing to find out how the macro played out.

I help companies build the operating discipline this demands — connecting AI-accelerated execution back to the one metric that governs survival. If your model is moving fast in every direction except toward cash, that's the conversation worth having.

Sources

- Hyperscaler AI capital expenditure. The four largest hyperscalers (Amazon, Alphabet, Microsoft, Meta) guided to roughly $725 billion in combined 2026 capital spending, up about 77% from a record ~$410 billion in 2025, per Financial Times earnings analysis (reported via Tom's Hardware and Yahoo Finance, 2026). Estimates range from ~$600B to ~$725B depending on which firms are counted and whether Oracle is included.

- Free-cash-flow impact. The scale of the buildout is sharply reducing hyperscaler free cash flow, with Amazon projected to turn free-cash-flow negative in 2026 (CNBC, February 2026).

- The zero-rate era. U.S. policy rates sat near historic lows for most of 2009–2021 before the 2022 tightening cycle reset the cost of capital (Federal Reserve, federal funds rate history).